Wealth of Advice, Swale House, Mandale Business Park, Durham, DH1 1TH

To help you make a more informed choice when it comes to your retirement – or at least to get an idea of the options you have available to you – we’ve put together this blog.

You can watch the video version of this blog post below, or keep on reading for more information about your retirement options.

The earliest you can take your pension is age 55, rising to 57 from 2028.

Usually, you can take up to a quarter of your pension tax-free, with the rest taxed as income when you take it out.

The options available from your existing pension may vary, but at a high level you have the option to exchange your pension for:

You always have the option to convert some or all of your pension savings to an annuity, which will pay you a guaranteed income for life.

At the start you can choose different options, like inflation protection or a continuing income for your partner or spouse after your death.

It’s important to get quotes from the whole market as different providers will offer the best rates at different times and make sure you confirm health and lifestyle details as these can boost your income.

A smoker for example, may be offered a higher income to account for a potentially shorter life expectancy.

Annuities can’t be changed once set up so you need to choose what’s right for you and get the best deal you can.

As an annuity has no investment element, this is why it is considered a lower risk option.

For a more detailed look at Annuities, you can download our free Guide to Annuities.

In contrast, drawdown lets you keep your pension invested and draw an income whenever you need to.

This means if you need more money than usual for whatever reason, you have the flexibility to take it, unlike with an annuity.

If your investments perform well and you don’t take too much out, you may have the ability to take higher income in the future. But the danger is you could run out of money if your investments perform poorly, you take out too much too early, or you live longer than expected.

This means it’s a higher risk option than an annuity, so it won’t be right for everyone.

We have an extensive guide to Income Drawdown available here.

With annuities and drawdown you take the tax-free cash at the start. With uncrystallised funds pension lump sums (UFPLS for short), it’s different. 25% of each lump sum is usually tax-free, with the rest taxable, while the remainder of your pension pot stays invested.

This means the risks are more like a drawdown plan and it’s a higher risk option than an annuity.

If you wanted to take £10,000 via UFPLS. £2,500 would be paid as Tax-free cash and £7,500 would be paid as taxable income.

Let’s say she’s single, 60 years old, and currently in receipt of a teacher’s pension which meets 90% of her expenditure.

Julie also has no children, so there’s no need to leave a legacy.

Her current pension pot is £200,000.

She uses £150,000 of this to purchase an annuity of £6,000 per annum, or £500 a month, and takes the tax-free lump sum of £50,000 to top up her cash balances.

This suits Julie’s requirements as she is happy to know she has a guaranteed income for life and an additional £50,000 lump sum, as well as her teacher’s pension.

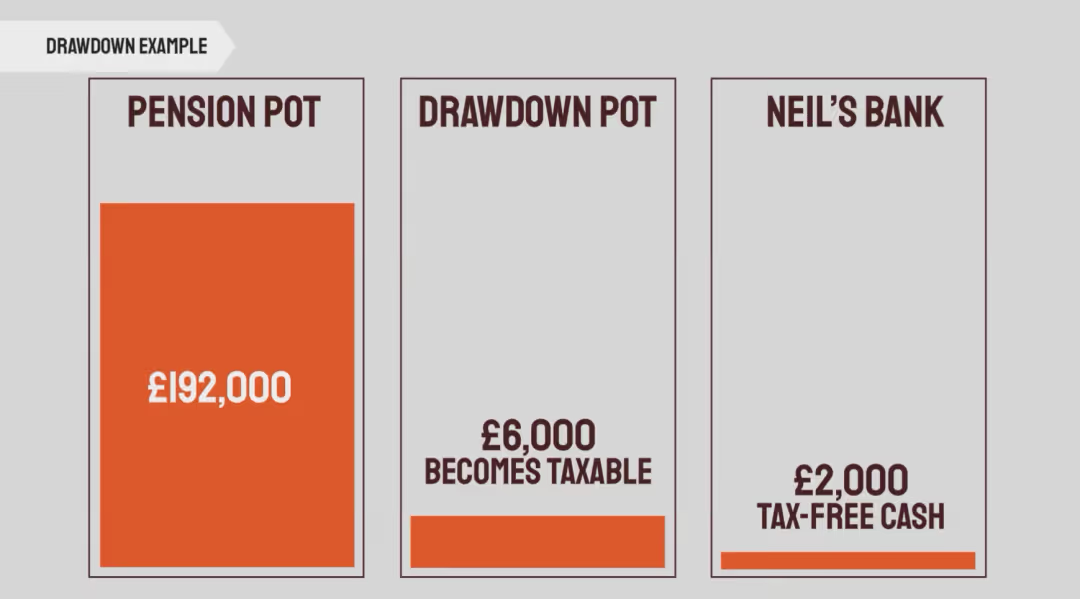

Neil is married, 55 years old and has a pension pot of £200,000.

Neil is an IT manager who has ‘retired’ but still intends to do a number of consultancy projects in retirement. Neil’s income will therefore vary and some months his consultancy work will cover his monthly expenses.

Neil would like a monthly income of £2,000 per month

As Neil does wish to start winding down and reducing his workload in retirement, he wants the ability to pick and choose what work he does. Neil also likes the idea of being able to have a month off work.

Drawdown suits Neil as he can turn on ‘income’ from his pension to match his expenditure needs.

Neil can choose to only take Tax-free cash from his pension, in order to ensure that no additional tax is taken from the income and also to ensure that he does not trigger the money purchase annual allowance (MPAA).

For every £2,000 worth of tax-free cash that he takes, £6,000 moves from Neil’s pre-retirement pot to his ‘drawdown pot’.

Michael is married, age 64 and already retired.

Michael worked in a factory and is due to take his Defined Benefit pension next year, from age 65. He also saved into a personal pension whilst working and has a pension of £200,000.

Michael’s wife Wendy has pension income which currently meets their regular expenditure.

Michael is keen to upgrade his car as he has been struggling to get in and out of his sports car recently.

In this tax year, Michael has the opportunity to benefit from UFPLS as he has no other income.

Michael could therefore access £16,760 from his pension via UFPLS without any tax being due.

25% is treated as Tax-free cash (£4,190) and the remaining 75% (£12,570) can be fully accommodated within Michael’s personal allowance.

The simple answer is to consider which of the options I have discussed will match your income objectives in retirement.

If you are low risk and cannot tolerate investment risk, then an annuity is the logical starting point.

If you are comfortable with investment risk, you can then consider if you would prefer a regular income stream to be paid for example monthly, or if you would prefer to take a lump sum or multiple lump sums throughout the year.

With both drawdown and UFPLS, it is important to consider the long-term sustainability of your pension.

The higher the level of withdrawals you take, the less chance that the income strategy will be sustainable throughout retirement.

So to recap, your three main options in retirement are an annuity, income drawdown or UFPLS. Whichever option you choose depends entirely on your personal circumstances.

There is also the option to blend all of the above options to suit your personal needs, depending on what you’re looking for in retirement.

Retirement is something that you only do once, and the decisions you make impact your income for the rest of your life – so it’s important to get it right.

I would always recommend at least discussing your specific options with a financial planner, who can help point you in the right direction.

Our initial meetings are free of charge, so it can’t hurt to ask!

You can get in touch with us by calling 0191 384 1008, emailing us at enquiries@wealthofadvice.co.uk, or alternatively by filling in the contact form we have on our website.

We’re authorised and regulated by the Financial Conduct Authority, and you can find us on their register with the number 563909.

The content of this blog is for educational purposes only, and should not be taken as personal advice. Retirement is a huge financial decision, so you should always discuss your options with a financial adviser before you make a decision.

If you want a better view of what your future could be, we'll have a chat and work out if we make a good fit for you and your financial picture.

Wealth of Advice are authorised and regulated by the Financial Conduct Authority, reference number 563909. This website is for information purposes only and is not personal advice.

We are committed to providing products and service of the very highest standards. If you feel that we haven't lived up to your expectations in any way, however, we would like to know so we can put things right for you. If you have a complaint, make sure you contact us directly. Accordingly, we will do all we can to resolve your complaint by the end of the next business day. However, if we can't do this, we will write to you within five working days to tell you what we have done to resolve the problem, or acknowledge your complaint and let you know when you can expect a full response. Furthermore, if we haven't issued our response within eight weeks from the date you first raised your complaint, or if you're dissatisfied with our response, you can ask the Financial Ombudsman Service - www.financial-ombudsman.org.uk - for an independent review. The Financial Ombudsman Service will only consider your complaint once you've tried to resolve it with us, so please take up your concerns with us first and we'll do all we can to help.

Wealth of Advice Ltd is a company registered in England and Wales, company number 07709624.

VAT Number: GB131946515