Wealth of Advice, Swale House, Mandale Business Park, Durham, DH1 1TH

The State pension is a political hot potato, due to its inflation ‘triple lock’ ensuring that it should keep pace with inflation.

Liz Truss had previously confirmed that the ‘triple lock’ would remain, and this would result in a 10.1% rise from April 2023, for those who are already in receipt of the State Pension. With a change in leadership, we’ll have to wait and see if Sunak and Hunt will honour this.

We’ve received a few questions from our clients about the state pension recently, so we wanted to put together this guide.

You can check your forecast by visiting the gov.uk website.

In order to qualify for the New State Pension, you will need a minimum of 10 years of National Insurance contributions.

To qualify for the maximum of £185.15 a week, you will need 35 full years of contributions.

The answer to this is, no there isn’t a problem.

It most likely means that you were ‘contracted out’ at some point.

Contracting out began in 1978 and ended in 2016, and it allowed people who were paying into a workplace or private pension to pay less national insurance towards their additional state pension, in exchange for getting a higher private pension.

If you were in a Defined Benefit Scheme it is likely that you were contracted out and your ‘missing State Pension’ is essentially in your Defined Benefit Scheme.

The good news is that having built up extra pension you can still build up 35 qualifying years to benefit from the full £185.15 per week.

Martin Lewis has estimated this could be worth thousands of pounds in extra income. There are lots of ifs and buts, because we don’t know how long you will live for, but for the cases we have looked at for clients it has always made sense to make the extra contributions.

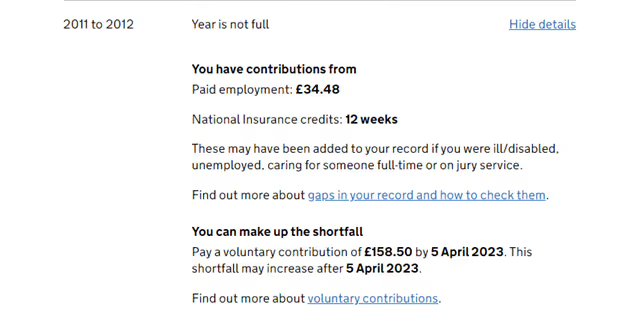

Looking through my own record, I have a ‘cheap year’ where I worked part-time at university. Rather than £825, it would only cost me £158.50 to top that year up to a full year.

If you need extra years to qualify, it makes sense to look through your record for any cheap years.

As you get closer to State Pension age, it becomes more relevant to review your records and to consider the voluntary contributions.

There are other activities that qualify for National Insurance such as Jury Service, Maternity, Paternity and Statutory Sick Pay.

One area that qualifies that is often overlooked is “Grandparents credits”, which the government call Specified Adult Childcare Credits.

You can benefit from this as long as you are:

I won’t go into all the rules and details in this post, but if you are retired and are looking after a family member who is under 12, you could consider if you are eligible for Specified Adult Childcare Credits.

You can apply for the Specified Adult Childcare Credits here.

You will receive a letter reminding you to claim, usually 2 or 3 months before you are due your first payment.

There are two ways to claim: there is an online form, or you can call the Pension Service Claim Line.

If you are still working, you can choose to defer. This means your state pension payments will increase by 1% for every 9 weeks that you defer, which works out at just under 5.8% for every 52 weeks. This can be a worthwhile option for those who don’t mind working for a bit longer.

Hopefully you found this guide helpful and informative, but if you have any questions or would like to suggest more topics for us to cover in this blog, please feel free to leave a comment below.

If you found this guide helpful, we also have a Guide to Understanding your Retirement Options available for free.

We’re a firm of Independent Financial Advisers based in the North East of England, who want to help people who’ve worked hard to get the retirement that they deserve. Our initial consultations are free of charge, and you can give us a call on 0191 384 1008 or email us your enquiry at enquiries@wealthofadvice.co.uk.

Wealth of Advice are authorised and regulated by the Financial Conduct Authority. You can find us on the Financial Conduct Authority register with the number 563909.

If you want a better view of what your future could be, we'll have a chat and work out if we make a good fit for you and your financial picture.

Wealth of Advice are authorised and regulated by the Financial Conduct Authority, reference number 563909. This website is for information purposes only and is not personal advice.

We are committed to providing products and service of the very highest standards. If you feel that we haven't lived up to your expectations in any way, however, we would like to know so we can put things right for you. If you have a complaint, make sure you contact us directly. Accordingly, we will do all we can to resolve your complaint by the end of the next business day. However, if we can't do this, we will write to you within five working days to tell you what we have done to resolve the problem, or acknowledge your complaint and let you know when you can expect a full response. Furthermore, if we haven't issued our response within eight weeks from the date you first raised your complaint, or if you're dissatisfied with our response, you can ask the Financial Ombudsman Service - www.financial-ombudsman.org.uk - for an independent review. The Financial Ombudsman Service will only consider your complaint once you've tried to resolve it with us, so please take up your concerns with us first and we'll do all we can to help.

Wealth of Advice Ltd is a company registered in England and Wales, company number 07709624.

VAT Number: GB131946515